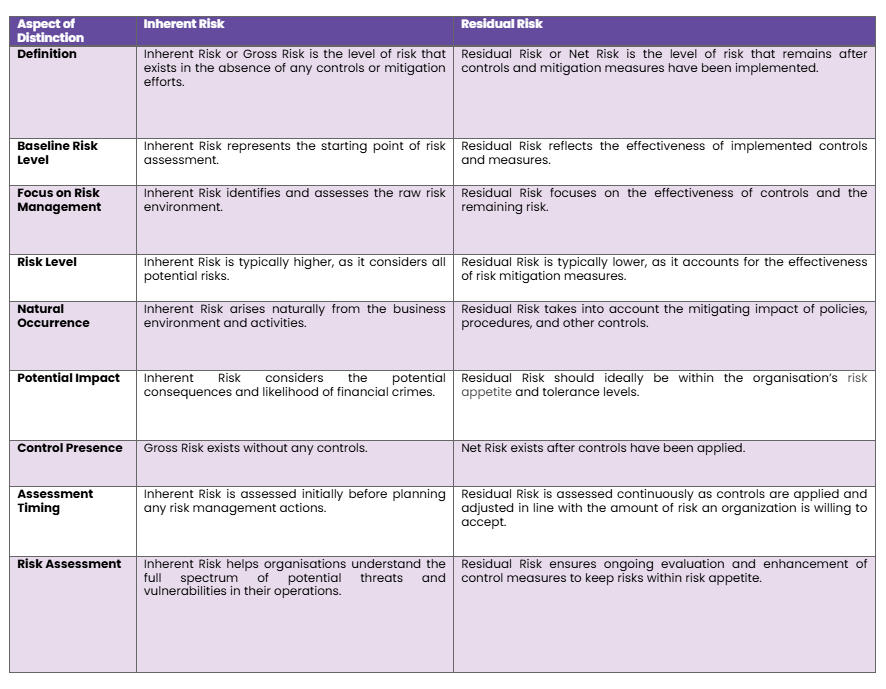

Compliance, in a general sense, means actions taken by individuals or organisations to follow laws, rules, policies, or guidelines that are expected to be followed. In case of non-compliance, they need to pay a price in the form of financial penalties, legal repercussions, and reputational damage. Financial Crime Compliance is a set of policies, procedures, and practices that the business needs to put in place in order to comply with and follow laws and regulations to prevent and detect financial crimes, such as money laundering (ML), Financing Terrorism (FT), fraud, corruption, proliferation financing (PF), etc.

Here’s a step-to-step approach to identifying residual risk to help businesses understand and manage their exposure to financial crime effectively.

The foremost step is analysing the business’s activities, products, and services to identify areas vulnerable to financial crimes, including ML, FT, and PF. Inherent risk emerges from various factors such as:

After identifying inherent risks, businesses need to assess and evaluate the likelihood and potential impact of each identified inherent risk, considering factors like regulatory environment, customer profiles, and geographic exposure.

Based on the assessment, businesses should rank the inherent risks. Such ranking can be based on their severity and likelihood, which would help businesses to focus on those that pose the greatest threat to the business. Risk prioritisation is based on the fundamentals of a risk-based approach (RBA).

After prioritising the risks, businesses need to identify control measures applied to fight against identified ML, FT, and PF risks. As part of this, they need to catalogue current AML and compliance measures, including policies, procedures, and technologies designed to mitigate identified risks

Based on the implementation and application of control measures, businesses must analyse the performance of existing controls through testing, audits, and reviews to determine how well they counter the inherent risks. Only then can businesses actually fill the gaps and analyse control effectiveness.

After evaluating the control effectiveness, all that is left is calculating the remaining risk, that is, residual risk. Such is determined by subtracting the effectiveness of existing controls from the assessed inherent risks, giving businesses a clear view of remaining ML, FT, and PF vulnerabilities.

Considering a situation where a Designated Non-Financial Business and Profession (DNFBP) named ABC Corp. needs to conduct an Enterprise-Wide Risk Assessment (EWRA).

A DNFBP conducts a thorough EWRA by considering factors such as customers, countries, staff and third parties and identifying risk scenarios to assess which ML, FT, or PF risks may materialise and what form they may take by assessing the impact on business. The impact on business was catagorised into low, medium, and high basis the loss or damage such risks would have on the business.

And conduct a thorough analysis of Scenarios to determine likelihood of occurrence and resulting impact for each probable scenario.

To mitigate risks identified, the DNFBP, ABC Corp. deployed various control measures such as:

Following which analysis of control measures was conducted for each scenario identified.

After implementing these measures, determination of residual risks is possible.

The DNFBP, ABC Corp. recognises that while it has taken significant steps to mitigate the identified risks, some risk still exists due to factors beyond its control. ABC Corp. is required to regularly monitor and evaluate control effectiveness

Managing residual risk in AML, CFT & CPF compliance is very important for businesses in mitigating potential ML, FT, or PF risks. Here’s an approach that lays down the basis for managing residual risk:

Defining the risk appetite gives clarity in the risk level that a business can take and its objectives related to financial crime compliance. For this purpose, businesses need to ensure that risk appetite aligns with overall business strategy and operational goals, as it cannot restrict or keep loose strands.

It is crucial for businesses to regularly review and assess current controls to identify any gaps and weaknesses. Based on the assessment, businesses need to customise existing controls by aligning them with best practices. When doing so, businesses need to keep in mind the specific residual risk of their business and operations.

As mentioned above, residual risk is the risk after employing effective measures; thus, for managing residual risk, it is essential for businesses to introduce new controls. Such new controls can include implementing new technologies and processes to address gaps identified.

Conducting ongoing assessments and monitoring of residual risk is essential for maintaining an effective compliance program. This involves continuously evaluating potential risks as new threats emerge as business operations evolve. Utilising key risk indicators and factors when undertaking ongoing monitoring and employing effective measures for dealing with residual risks allows for timely adjustments to the compliance strategy.

Staff training is fundamental to an effective compliance program. Regular training sessions should cover compliance procedures, emerging threats, and the importance of individual roles in the compliance framework. Creating awareness through training fosters a culture of compliance, empowering employees to identify any suspicious activities.

Managing residual risk is important to keep the business in check. When assessing residual risk, if there is any suspicion, businesses need to promptly report it to their regulatory authorities. Businesses should also keep checking and streamlining the process of submitting Suspicious Activity Reports (SARs) and Suspicious Transaction Reports (STRs) on the goAML portal. In doing so, they need to ensure that the submission process is efficient and compliant with regulatory requirements for timely reporting. As part of this, businesses need to look over and manage residual risk by monitoring submission trends that can provide insights for improving the compliance framework.

Investing in comprehensive AML software is crucial for integrating various compliance functions. When choosing AML software for managing residual risk, businesses should employ robust and customisable, allowing them to tailor it to their specific risk profiles and operational needs. A well-integrated AML solution enhances the efficiency and effectiveness of the compliance program and also continuously helps to identify and manage any ML, FT, and PF risks.

Leveraging data analytics is essential for uncovering hidden patterns that may indicate financial crime, including ML, FT and PF-related crimes. Advanced analytics tools and technology can identify correlations and trends that manual processes might overlook. Regular reviews of these analytics methods will help businesses stay ahead of emerging risks, allowing for proactive adjustments to their compliance strategies.

Conducting periodic health checks on the compliance program is key to ensuring its ongoing effectiveness. These assessments evaluate whether the current policies, controls, and procedures remain relevant and efficient or if there are any gaps in their effectiveness. As part of health checks, businesses should benchmark against industry standards to identify areas for improvement and enhance overall compliance performance.

Engaging independent auditors to review the compliance program adds an extra layer of assurance to the AML/CFT framework’s effectiveness. These audits provide an objective assessment of the effectiveness of financial crime compliance measures. The findings from independent audits should be used to drive enhancements, ensuring that the compliance program evolves in response to new challenges.

Regularly reviewing and enhancing the AML/CFT program is a must for adapting to the changing regulatory framework and evolving risks. This includes evaluating existing policies, procedures, and controls to ensure they are effective and up-to-date. Implementing necessary enhancements will strengthen the overall compliance framework.

Collaborating with industry peers provides valuable insights and best practices in managing financial crime risks, including ML, FT, and PF. Sharing information on emerging threats and effective strategies enhances collective knowledge and strengthens the overall industry response to financial crime.

Active engagement with regulatory bodies is essential for staying informed about compliance requirements and expectations. Businesses should establish open lines of communication with regulators, ensuring that they are aware of any changes in regulations and can adapt their compliance programs accordingly.

The risk-based approach (RBA) requires entities such as DNFBPs to deploy ML, FT, and PF risk mitigation in proportion to the extent to which ML, FT, and PF are exposed. RBA can be used to effectively manage residual risk due to the following reasons:

By identifying and prioritising residual risks, businesses can allocate resources to the areas that pose the greatest remaining threat, optimising their compliance efforts.

Even after controls are in place, a risk-based approach facilitates the ongoing identification of new or evolving risks, ensuring that residual risks are continuously monitored and addressed.

Businesses can adjust their compliance strategies in response to changes in the ML, FT, PF, and other financial crime risks, ensuring that residual risks are effectively managed as circumstances evolve.

By focusing on residual risks, businesses can enhance their compliance with AML/CFT regulations, ensuring that they remain vigilant even after initial controls are applied.

The ability to quickly adapt to new information about residual risks allows businesses to respond more effectively to potential financial crime threats.

Analysing residual risks using a risk-based approach provides critical insights that guide management decisions regarding additional controls or modifications to existing ones, enhancing overall risk management.

Understanding and managing residual risks is essential for demonstrating compliance with regulatory expectations, reducing the likelihood of violations even after implementing controls.

A risk-based approach helps in effectively managing residual risk and helps safeguard the business’s reputation, as proactive measures convey a commitment to ethical standards and compliance.

The risk-based approach allows for the development of specific controls targeting identified residual risks, enhancing their effectiveness and relevance.

Training programs can be designed to address the specific residual risks faced by the business, ensuring that employees are prepared to handle these challenges effectively.

By implementing Risk-Based Customer Due Diligence (CDD) procedures, businesses can focus their efforts on high-risk clients, mitigating residual risks associated with less scrupulous actors.

Maintaining a clear framework for understanding and managing residual risks fosters transparency within the business organisation and builds trust with regulators and clients.

Proactively addressing residual risks reinforces stakeholder trust, as it demonstrates a commitment to effective risk management and ethical business practices.

Here is the list of challenges usually faced by businesses in managing residual risk:

ML/FT & PF typologies are dynamic in nature, constantly changing as criminals adapt their methods. This evolution can be driven by advancements in technology or changes in the financial market. As a result, businesses face the challenge of keeping their risk assessments relevant and effective, as outdated information can lead to undetected risks.

With dynamic ML/FT typologies and to combat them, regulation needs to be amended, making the regulatory environment surrounding financial crimes dynamic, with frequent updates and new requirements. Businesses need to navigate a complex landscape of laws, which also vary based on jurisdiction. This constant flux in the regulatory framework can lead to confusion, leaving businesses open to non-compliance if they fail to keep a pace that exposes them to ML, FT, and other financial risks.

For any cross-border multinational organisation, following differing regulations across countries is necessary and can complicate compliance efforts. Each jurisdiction has its own AML rules, which can create a patchwork of requirements that are difficult to manage. This complexity can lead to gaps in compliance and increased vulnerability to ML, FT, and PF risks.

Businesses operate under budgetary and staffing limitations, which can hinder their ability to implement effective risk management practices. Limited resources may result in inadequate AML compliance functions and ineffective technology solutions. This scarcity can ultimately leave businesses exposed to ML, FT, and PF risks they cannot adequately address.

Data silos occur when information is isolated within specific systems, preventing a holistic view of risk. This fragmentation can obscure insights and hinder collaboration, making it challenging to identify trends or correlations that could indicate risk. The lack of comprehensive data integration can lead to blind spots in risk management efforts.

Data quality can severely impact risk assessments and compliance efforts. Poor, inaccurate, incomplete, or inconsistent data can lead to misguided conclusions and decisions. The reliance on large volumes comprising poor-quality data makes it difficult to ensure high standards of data integrity across and in the AML compliance implementation measures.

Many businesses rely on outdated legacy systems that may not support current risk management needs. These systems can be inflexible, difficult to integrate with new technologies, and incapable of processing modern data requirements. The reliance on legacy systems can impede the business’s ability to respond to emerging risks effectively.

Transaction monitoring systems are prone to high rates of false positives, which can overwhelm compliance teams, leading to inefficiencies and a significant drain on resources. When too many alerts are triggered, it can create alert fatigue, causing critical risks to be overlooked or deprioritized. This reduces the effectiveness of compliance efforts and undermines staff morale.

Residual risk requires implementing new controls or procedures often meet with resistance from staff. This resistance can stem from a fear of change, a lack of understanding of new processes, or the perception that additional compliance requirements increase their workload. Such resistance can hinder the adoption of necessary changes, ultimately impacting the effectiveness of risk management efforts.

Regulated Entities such as DNFBPs can manage residual risk through the implementation of the following best practices:

Conduct comprehensive risk assessments on a regular basis to identify and evaluate potential risks across the business. This proactive approach helps adapt to evolving threats and ensures a consistent understanding of the risk landscape.

Implement robust internal controls that are tailored to the business’s specific risk profile. These controls should address key vulnerabilities and ensure compliance with regulatory requirements.

Regularly test and review the effectiveness of controls to identify any weaknesses. Utilise key performance indicators to monitor control performance and make necessary adjustments.

Leverage technology to automate routine compliance and monitoring tasks. Automation can enhance efficiency, reduce human error, and allow staff to focus on higher-level analysis and decision-making when managing residual risks.

Leverage technology to automate routine compliance and monitoring tasks. Automation can enhance efficiency, reduce human error, and allow staff to focus on higher-level analysis and decision-making when managing residual risks.

Leverage technology to automate routine compliance and monitoring tasks. Automation can enhance efficiency, reduce human error, and allow staff to focus on higher-level analysis and decision-making when managing residual risks.

Prioritise data quality through governance practices, validation processes, and regular audits. High-quality data is essential for accurate risk assessment and compliance efforts.

Establish continuous monitoring systems to detect anomalies and assess risk in real time. This allows organisations to respond promptly to potential threats before they escalate.

Conduct independent audits of risk management practices and compliance programs to provide an objective assessment of their effectiveness. Audits help identify areas for improvement and reinforce accountability.

Invest in regular training programs to ensure staff understand their roles in risk management and compliance. Foster a compliance culture that emphasises the importance of vigilance and ethical behaviour.

Ensure that senior management is actively involved in risk management efforts. Their commitment and oversight are crucial for setting the tone at the top and ensuring alignment with strategic objectives.

Develop and communicate clear policies and procedures related to risk management and compliance. This provides staff with a framework for understanding their responsibilities and ensures consistency in execution.

Clearly articulate the business’s risk appetite to guide decision-making and resource allocation. A well-defined risk appetite helps align risk management strategies with the business’s overall objectives and ensures a balanced approach to risk-taking.

Future Trends and Development for Residual Risk Management in AML, CFT and CPF Compliance.

AI will play a crucial role in enhancing fraud detection and compliance processes. By leveraging AI algorithms, businesses can automate the identification of suspicious activities, analyse patterns, and reduce false positives, ultimately streamlining compliance operations.

Machine learning models will continuously improve risk assessments by learning from historical data. These models can adapt to evolving financial crime tactics, enhancing the accuracy of predictions and helping institutions stay ahead of emerging threats.

Blockchain technology offers a transparent and immutable ledger that can enhance traceability in financial transactions. Its application can help verify the authenticity of transactions and reduce the risk of fraud, thus strengthening compliance measures.

RPA can automate repetitive tasks such as data entry and reporting, allowing compliance teams to focus on more strategic activities. By improving efficiency, RPA helps manage residual risks more effectively and reduces the likelihood of human error.

The integration of big data analytics enables businesses to analyse vast amounts of data from various sources. This holistic view helps identify potential risks and anomalies that may indicate financial crime, allowing for proactive measures to mitigate those risks.

As financial crimes become more sophisticated, regulators are tightening compliance requirements. Businesses will need to adopt more robust residual risk management frameworks to meet these evolving standards and avoid hefty penalties.

Collaboration between public institutions and private businesses can enhance intelligence-sharing regarding financial crime trends. These partnerships can lead to more effective strategies for managing residual risks and improving overall compliance frameworks.

The development of dynamic models that can adjust in real time to reflect changes in risk profiles. This agility will enable businesses to respond promptly to emerging threats and manage residual risks more effectively.

Regular scenario analysis and stress testing will become integral in understanding potential impacts of financial crime. Businesses will simulate various scenarios to gauge their risk exposure and develop mitigation strategies accordingly.

Strengthening governance frameworks will be essential for managing residual risks. This includes establishing clear roles, responsibilities, and accountability mechanisms within businesses to ensure effective compliance and risk management.