How to File CNMR and PNMR on the goAML Portal Under TFS Guidance, 2025

How to File CNMR and PNMR on the goAML Portal Under TFS Guidance, 2025

- Fund Freeze Report (FFR) changed to Confirmed Name Match Report (CNMR)

- Clarified screening during weekends and public holidays

- Updated procedures related to Partial Name Match Reporting

- Additional examples on PNMR Reporting

- Grievance procedures were deleted and published separately on the EOCN website.

The blog also includes a detailed explanation of what TFS obligations are, an in-depth understanding of CNMR and PNMR filing obligations and step-wise processes under TFS Guidelines 2025, and the best practices that Reporting Entities can incorporate into their AML framework to ensure Sanctions Compliance.

Apart from procedural updates, this blog also provides a step-by-step walkthrough for CNMR and PMNR filing using the goAML portal, helping AML compliance professionals and Regulated Entities to understand their core TFS compliance obligations.

Guidance on Targeted Financial Sanctions, July 2025: What Reporting Entities Must Know

What are Targeted Financial Sanctions (TFS) in the UAE?

“Targeted Financial Sanctions” refers to an obligation to freeze the funds or other assets of designated individuals or entities, and to restrict access to such funds, assets, or related services, either directly or indirectly.

The primary purpose of TFS is to prevent designated persons and entities from accessing financial resources, thereby disrupting the use of such resources for illicit purposes or transactions that may benefit individuals or organisations involved in terrorism, proliferation financing, or other criminal activities.

TFS Compliance Obligations

Register

- The UAE Local Terrorist List that contains the names of all the sanctioned individuals, entities, or groups designated by the UAE Cabinet.

- The UNSC Consolidated List that contains the names of all the sanctioned individuals, entities, or groups designated by the United Nations Sanctions Committees or directly by the UNSC.

Screen

The “when” and “whom” of sanctions screening is covered under paragraphs 30 and 31 of the latest guidance, which provide that Reporting Entities must undertake regular and ongoing screening on the latest Sanction Lists. Sanctions Screening must be undertaken mandatorily in the following circumstances:

- Updates, i.e., additions, deletions, and revisions of names to Sanction lists

- Prior to onboarding a new customer, i.e., a potential customer

- Persons or entities party to any transactions or related to parties of any transaction, including names of persons with direct or indirect relationships with designated individuals, entities, or groups

- Upon periodic KYC reviews or if there is any material change in the nature or ownership of the customer is identified

- Daily screening of the existing customer database

- Daily screening of the offboarded customers or previous customers with whom the Regulated Entity had prior business relationships and transactions

- Reporting Entities need to be mindful that they are required to SCREEN all their previous or offboarded customers on an ongoing basis for a period of five (5) years after termination or cessation of the business relationship, even if there is no active business relationship or no assets are held with the Regulated Entity at present.

- Before processing any transactions with a counterparty.

The “what” of the sanctions screening requirement is covered under paragraphs 32 and 33, which state the “key identifiers” and “other identifiers” required to be obtained by regulated entities from their customers to screen their names against those contained in the latest sanctions lists. These key identifiers and other identifiers are:

- Confirmed Name Match: The name of the customer matches with the sanctions screening outcome.

- Partial Name Match: The name of the customer partially matches with the sanctions screening outcome.

- False Positive: The name of the customer does not match with the screening outcome.

- Negative Match: The name of the customer does not generate a screening outcome.

| Sanctions Screening Outcomes and Resultant Reporting Requirements | |||

| Screening Result | TFS Measures | TFS Reporting Requirement | Record-Keeping Obligation |

Perfect Match or Confirmed Name Match |

| Confirmed Name Match Report (CNMR) to be filed within 5 days alongwith obligatory information |

Paragraph 46 of the TFS Guidance updated in July 2025 prescribes to maintain records for the duration of atleast five (5) years, irrespective of the screening outcome. |

| Partial Match |

| Partial Name Match Report (PNMR) to be filed within 5 days alongwith obligatory information | |

| False Positives or False Match | Not applicable | No reporting required | |

| No Match or Negative Match | |||

Implement TFS Measures

- Asset Freezing without delay

- Prohibition from making funds or other assets or services available

- Financial Assets

- Economic Resources

- Any other assets.

Report

- Confirmed Name Match Report (CNMR)

- Partial Name Match Report (PNMR)

The TFS Guidance also requires Reporting Entities to include and enclose mandatory and obligatory information along with the CNMR and PNMR filed.

In the context of CNMR, the RE is required to enclose ID documents of the person or legal entity whose name is found in the sanctions lists, resulting in a confirmed match during screening, as without possession of ID documents, the RE cannot conclusively confirm that the screening match found is a perfect match, requiring regulatory reporting. Examples of obligatory information for CNMR are:

- The amount of funds or other assets frozen with documentary evidence, such as bank statements, transaction receipts, investment portfolios, title deeds, account summaries, etc

- Detailed description of rejected transactions or services.

- Funds or other assets that are suspended

- Detailed description of rejected transactions or services.

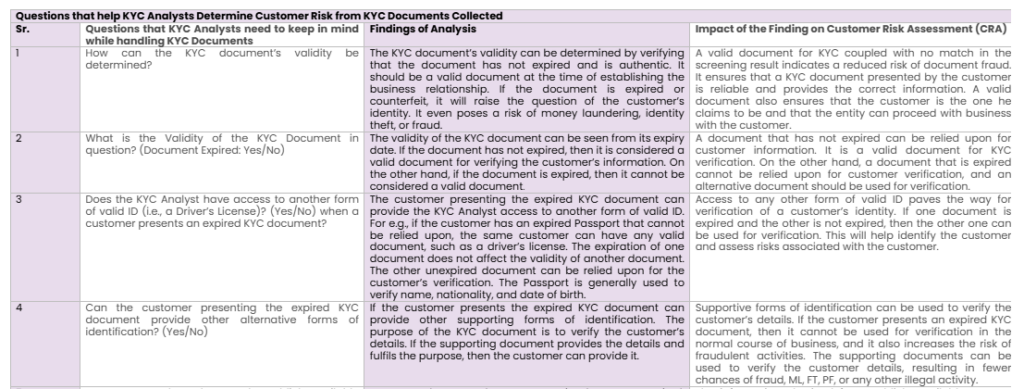

How to File a Confirmed Name Match Report (CNMR) While Implementing TFS Measures

Identification of Confirmed Name Match During Sanctions Screening

REs can opt to screen their customers manually across the Sanctions Lists obtained through NAS or rely on a Sanctions Screening Software or unified AML Software that relies on efficient Screening APIs. Using one of these or a combination of software tools ensures that Sanctions Lists relied on for screening customers are updated in real time as published by the regulator, or EOCN, in the context of TFS compliance. The process of screening customers generates screening results or screening outcomes, which need to be disambiguated by the Screening Analyst.

Regulated Entities must remain mindful that they screen across their customer databases, which include potential, existing, and former customers, with whom they had a previous business relationship during the past five (5) years

When a Screening Analyst, while disambiguating screening results, identifies a perfect match or a confirmed match, they need to assess the screening outcome to confirm its accuracy.

Assessment of Confirmed Name Match Outcome

Escalation by the Frontline Team or Screening Analyst to the AML Compliance Officer

Impose Freezing Measures on Potential, Existing, and Former Customers

In case of a Potential Customer

- Rejection of transaction or service immediately

In case of a Potential Customer

- Freeze all funds/assets

- Prohibition from making funds, other assets, or services available to such customer

In case of a Potential Customer

- If the confirmed match is that of a former customer and the RE does not have any assets or funds available with them, they can still proceed with the CNMR filing process, stating that business relationship concluded and they are not in possession of any assets.

Preparation of Mandatory and Obligatory Information & Documents for CNMR in alignment with goAML Requirements

- Asset value proof (bank statements, portfolio summaries, title deeds)

- Description of rejected service or transaction.

Logging in on the goAML Portal to File CNMR

Selecting Report Type as CNMR & Entering Information and Documents

Saving and Submitting CNMR

Maintaining Records of CNMR Filed for Five (5) Years

How to File a Partial Name Match report (PNMR) While Implementing TFS Measures

Identification of Partial Name Match During Sanctions Screening

Regulated Entities must ensure that they screen across their customer databases, including potential, existing, and former customers, with whom they had a previous business relationship during the past five (5) years.

When a Screening Analyst, while disambiguating screening results, comes across screening results or outcomes where only some or few of the attributes of the customer profile, and they cannot conclusively confirm whether or not such a match is a confirmed match or a false positive, then in such a scenario, they are required to escalate the customer profile and screening outcome to the AML Compliance Officer for further assessment.

Assessing Partial Name Match Outcome

- Lack of adequate information and non-availability of the customer’s ID documents in case of potential customers

- Lack of information in Screening Outcomes, i.e., screening results exist but don’t provide adequate information so as to conclude successful disambiguation

- A high number of screening outcomes or results are generated by the screening software due to lower match percentage thresholds configured, leading to high disambiguation volume with non-existent substantial information for disambiguation.

In order to simplify the Partial Name Match Outcome’s accuracy assessment, the following factors must be considered by Reporting Entities, such as:

For Potential Customers: Obtaining ID documents must be attempted when ID documents are not available, leading to a lack of information on key identifier details, so that the match can be disambiguated by having a complete set of information prior to disambiguation for accurate results.

- If ID is received within 10 days, the RE must conduct Screening with details contained in the ID obtained. Based on the screening outcome, if the RE finds that the match is indeed a Partial Match, they must continue/implement Suspension/Freezing Measures and proceed with the PNMR/CNMR filing process. If, after fresh screening, the RE finds that the screening outcome is a false positive or no match, they must proceed with establishing a business relationship.

- If ID is not received within 10 days, the RE must Reject/Cancel Transaction and proceed with PNMR filing process

- If ID is received after 10 days, the RE must conduct Screening based on the recently acquired ID and implement Suspension Measures accordingly, if a Partial Match is found, or proceed with CNMR if a Complete Match is found, or establish a business relationship if false or no match found.

Existing and Former Customers: The possession of a Customer ID is assumed

- Suspend any transaction, refrain from offering any funds, assets, or services.

Escalation by the Frontline Team or Screening Analyst to the AML Compliance Officer

Impose Suspension Measures on Potential, Existing, and Former Customers

In case of a Potential Customer

- Cancel the Transaction and proceed with the PNMR filing process

Existing and Former Customers

- Suspend any transaction, refrain from offering any funds, assets, or services.

Preparation of Mandatory and Obligatory Information & Documents for CNMR in alignment with goAML Requirements

- Asset value proof (bank statements, portfolio summaries, title deeds)

- Description of suspended service or transaction

- Description of rejected transaction or service (when no funds are held).

Logging in on the goAML Portal for PNMR Filing

Selecting Report Type as PNMR & Entering Information and Documents

Saving and Submitting PNMR

Following EOCN Response

REs after filing a PNMR must await and follow the EOCN instructions and maintain suspension measures until further instructions are received.

The EOCN instructions in the context of PNMR concern the treatment of suspension measures, particularly in the case of existing and former customers. The Reporting Entity must submit PNMR along with all the necessary and obligatory customer information so that EOCN can verify the PNMR submitted and give further instructions to the RE. Either of the following steps must be taken by RE, based on EOCN response:

- If EOCN concludes PNMR filed as a False Positive, RE must cancel TFS suspension measures and proceed with the business relationship

- If EOCN validates PNMR as a Confirmed Match, REs must freeze funds and submit CNMR.

Maintaining Records of PNMR Filed for Five (5) Years

Key Differences Between CNMR and PNMR: Comparative Table

Differences Between CNMR and PNMR | ||

| Distinguishing Aspects | CNMR (Confirmed Name Match Report) | PNMR (Partial Name Match Report) |

| Trigger Event | Identification of Confirmed Match during Sanctions Screening | Identification of Partial Match during Sanctions Screening |

| Immediate Action Needed | Freezing Measures for TFS Compliance to be applied within 24 hours | Suspension Measures for TFS Compliance to be applied within 24 hours |

| Filing Timelines | Within 5 days after imposing Freezing Measures | Within 5 days after imposing Suspension Measures |

| Documents Required | Complete Customer ID + Documents of Freezing Measures/ Transaction Rejection | Complete or Partial Customer ID + Documents of Suspension Measures |

| Post Filing Measures | Freezing Measures to say in place. However lift Freezing Measures if Person/Entity is Delisted from Sanctions List or Freezing Cancellation Decision given by EOCN | Await EOCN Response, maintain Suspension Measures, may need to file CNMR or mark match as False Positive |

Key Differences Between Freezing and Suspension Measures

Differences Between Freezing and Suspension of Funds | ||

Distinguishing Aspects | Freezing Measures | Suspension Measures |

Sanctions Screening Disambiguation Outcome | Confirmed or Perfect Match | Partial Match |

Report to be filed on GoAML Portal | CNMR | PNMR |

TFS Compliance Requirements | Freezing measures remain in place until person/entity is delisted from Sanctions List or Freezing Cancellation Decision given by EOCN | Suspension measures remain in place until EOCN provides further instructions on the match’s status |

General Do’s and Don’ts to Ensure TFS Compliance

Dos to Ensure TFS Compliance

Do subscribe to the Executive Office mailing list or alert system

Regulated Entities (DNFBPs, VASPs, and FIs) are required to register on the goAML platform to submit STRs and SARs to the FIU. They must also use the platform to report CNMRs/PNMRs to the EOCN and the Supervisory Authority.

Do screen continuously, even on weekends and holidays

Reporting Entities must establish internal procedures for screening against the UAE Local Terrorist List and UNSC Consolidated List during weekends and public holidays, ensuring that access to funds or assets is restricted at all times. If no transactions or customer access occur during weekends or holidays, screening must begin immediately at the start of business activity, and freezing measures should be promptly applied.

Do Report and Disclose previous transactions or business dealings with Confirmed or Partial Name Matches.

Reporting Entities must submit CNMRs and PNMRs for all relevant transactions, business relationships, and accounts held within the past five years, including those closed before the designation, even if no current assets or ties exist. The report must explicitly state that no funds or assets are presently held, no ongoing relationship exists with the designated party, and that the account in question is closed.

Do Report Matches via Email to the EOCN if You’re Not a goAML User

For an entity not registered with goAML (that do not fall under the definition of FIs, DNFBPs, or VASPs and are therefore not under an obligation to register on goAML), CNMRs or PNMRs must be reported by emailing and providing a complete set of case details that clearly explain the identified match with all relevant supporting documents attached in the message.

Do Escalate Matches Found in Criminal or Unilateral/Multilateral Sanctions Lists

Reporting Entities must consult the relevant Supervisory Authority (SA) for guidance on handling matches found with unilateral or multilateral sanctions lists, or other criminal lists, and consider submitting an STR or SAR to the Financial Intelligence Unit (FIU) if such matches are confirmed. The Reporting Entity should not use CNMR/PNMR reports in goAML for matches found on other sanction or criminal lists like OFAC, EU, HMT, or INTERPOL. These reports are only for matches with the UAE Local Terrorist List and UN List.

Do understand the change in penalty for non-compliance and inform staff

Reporting Entities must equip themselves with the awareness of changes made to the penalty imposed on TFS violations and incorporate the changes, such as imprisonment for a period of one to seven years. REs must also understand that Administrative Sanctions might be applied to them, resulting in a warning for license cancellation.

Don'ts to Ensure TFS Compliance

Don’t overlook changes in ownership structures, as even minority holdings may evolve into controlling stakes.

Reporting Entities are required to impose freezing measures on any entity that is majority-owned (more than 50%) by designated persons or entities. During implementation, REs must determine whether a designated person owns or exercises control over more than 50% of the proprietary rights. If the designated individual holds only a minority stake (50% or less), the entity is not subject to freezing measures unless ownership shifts, and the designated person gains a majority stake or controlling interest. Furthermore, all funds or assets owed to designated individuals must be frozen and must not be made accessible under any circumstances.

Don’t notify customers before freezing measures, as doing so may be considered tipping off

Reporting Entities must avoid informing customers about freezing measures before they are applied, as this may constitute tipping off. Customers may be notified once the measures have been implemented.

Don’t Forget to Document False Positives

Reporting Entities do not need to report a False Positive result to the EOCN and may proceed with the business transaction. However, they must maintain internal records of the screening alert and all actions taken.

Don’t rely solely on third-party screening services to meet compliance obligations

Reporting Entities must not consider third-party screening services as a guarantee of compliance. Reporting Entities remain responsible and must assess the reliability and robustness of external systems before using them.

Don’t Rely on Assumptions or Unverified Links

When a Confirmed or Partial Name Match is identified, the Reporting Entity must obtain and review the customer’s identification documents. Following the review, appropriate freezing or suspension actions should be taken and properly documented.

Best Practices for CNMR and PNMR Filing on the goAML Portal to Ensure TFS Compliance

Establish Comprehensive Sanctions Compliance Policies and Internal Controls

Using Sanctions Screening Software for Accuracy

Providing Sanctions Compliance Training to Employees

Group Oversight Across All Branches and Trade Zones

Tamper-Proof Record-Keeping

Implementing Centralised Record Management Systems

Internal Reporting & Escalation Module

Bringing It All Together: TFS Measures, Match Outcomes, and goAML Reporting

The advent of TFS Guidance, July 2025, calls for more than reactive and passive compliance measures; it requires proactive internal policies and procedures that take care of timely screening, clear escalation protocols, and accurate CNMR/PNMR reporting through the goAML portal and reposting to the relevant Supervisory Authority. Irrespective of dealing with confirmed or partial match in case of potential, existing, or former customers, regulated entities must implement appropriate freezing or suspension measures, document actions taken, and maintain records for a period of five (5) years.

Incorporating these practices into daily workflows helps ensure regulatory compliance while reinforcing operational resilience. With right Sanctions Screening Software, Role Specific AML Training, and governance, REs in UAE can go beyond reactive compliance and master proactive and risk-based TFS Compliance.

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is a Chartered Accountant with more than 26 years of experience in governance, risk, and compliance. He helps companies with end-to-end AML compliance services, from conducting Enterprise- Wide Risk Assessments to implementing the robust AML Compliance framework. He has played a pivotal role as a functional expert in developing and implementing RegTech solutions for streamlined compliance.